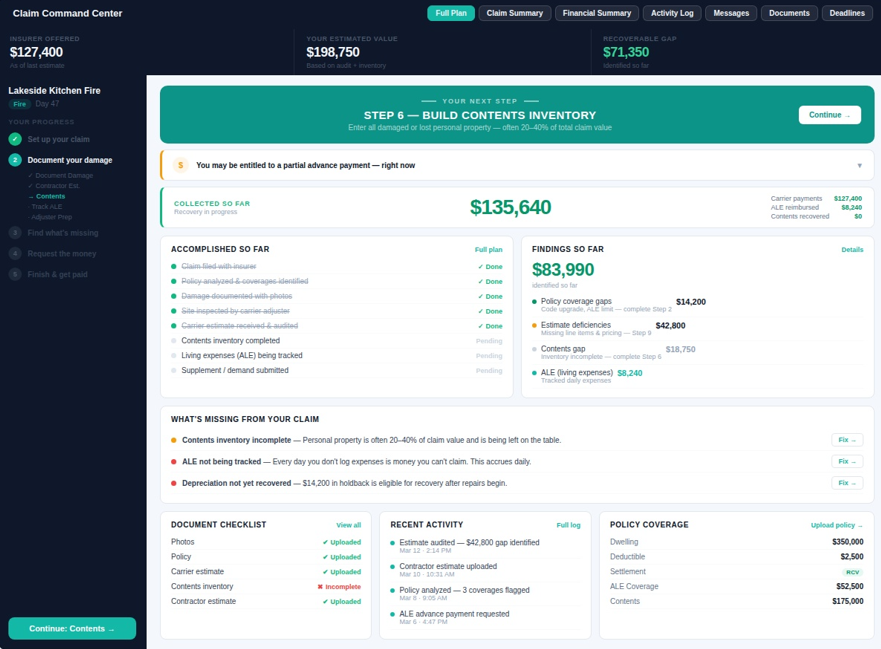

The Claim Command Center

This puts you in control of your claim — not just responding to it.

Start here. This is where your claim process begins.

You always know where you are

Five phases — Set Up Your Claim, Document Your Damage, Find What's Missing, Request the Money, Finish & Get Paid. The Command Center lays out every step in order with clear status, so you always know where you are and what comes next.

Every step tells you what to do

Each step explains why it matters, exactly what action to take, and what Claim Command Pro gives you to complete it. You're never left to figure it out on your own.

The system does the hard work

Policy review, estimate analysis, and claim documentation are handled for you — producing structured outputs similar to what claim professionals generate.

What You Actually Get

Not just reports. Not just advice.

Claim-ready documentation you can send directly to your insurer.

- ✓ Professional supplement requests

- ✓ Formatted dispute letters

- ✓ Organized damage documentation

- ✓ Step-by-step claim guidance

What isn't documented doesn't get paid.

What you don't question doesn't get reviewed.